For years, the most aggressive competition in private markets centered on technology, platforms, and growth narratives. That era is losing momentum.

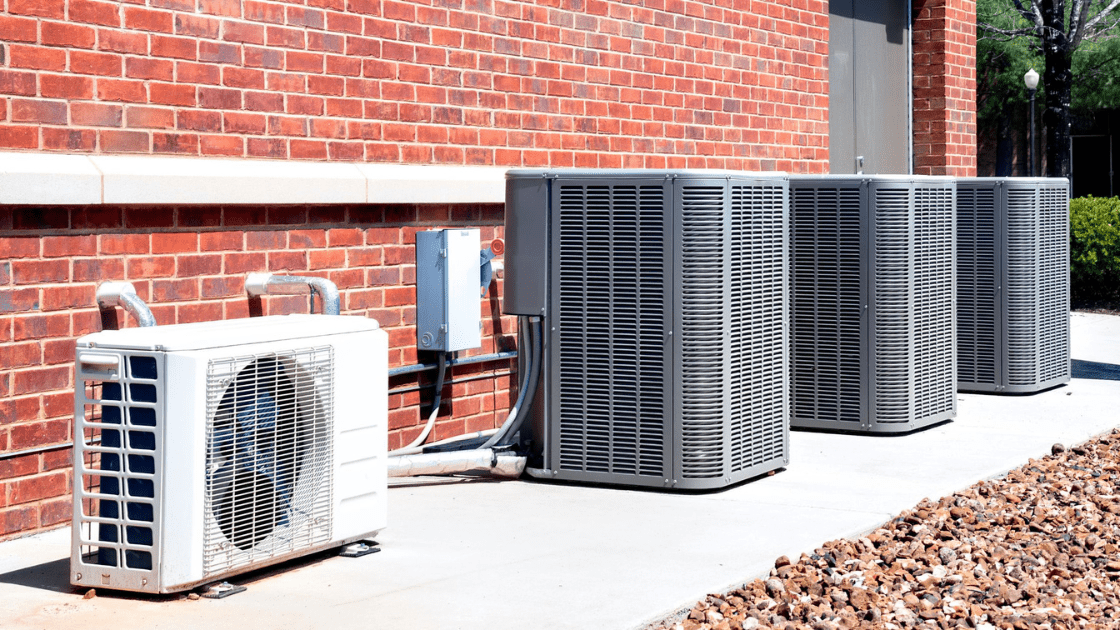

Today, some of the most contested deals are far less visible: HVAC platforms, regional logistics operators, healthcare services firms, specialty manufacturers, and unglamorous B2B service businesses with steady cash flow and modest growth.

These businesses rarely dominate headlines. Yet they are increasingly at the center of bidding wars between family offices and traditional private equity.

This shift is not a tactical rotation. It reflects a deeper realignment in how sophisticated capital evaluates risk, return, and time.

Historically, these assets sat squarely within private equity’s comfort zone. Predictable EBITDA, fragmented markets, limited disruption risk, and clear operational levers made them ideal buyout candidates.

What has changed is not the businesses themselves. It is the buyer.

Large family offices are no longer passive allocators relying on PE funds to access these opportunities. Many now resemble institutional investors in their own right, with capital bases comparable to lower middle-market firms but without fund-life constraints.

That structural difference matters.

HVAC systems fail regardless of economic cycles. Freight continues to move. Healthcare services remain essential. Specialty manufacturing and B2B services are embedded in supply chains that do not pivot overnight.

These characteristics create durability. And durability has become increasingly scarce.

For family offices, these businesses offer something growth assets often do not: predictability. Cash flow is visible. Pricing power is defensible. Customer churn is low. Value compounds through operational discipline rather than financial engineering.

Private equity, by contrast, is often constrained by defined investment horizons and return optics. Many of these businesses do not optimize for speed. They optimize for continuity.

Family offices can accept lower headline IRRs in exchange for certainty, control, and long-term compounding. They can hold assets indefinitely, reinvest through cycles, and prioritize governance over exit timing.

In competitive processes, that flexibility allows them to outbid traditional PE without overpaying in economic terms.

This dynamic is reshaping the lower middle market. Assets once viewed as mundane are now increasingly scarce. And scarcity changes perception.

Boring businesses are becoming luxury assets.

Not because they are glamorous, but because they offer something increasingly rare in modern capital markets: durable cash flow, pricing power, and low volatility without reliance on narrative-driven growth.

Explore partnership opportunities with an editorial distribution platform reaching 1.8M+ people monthly