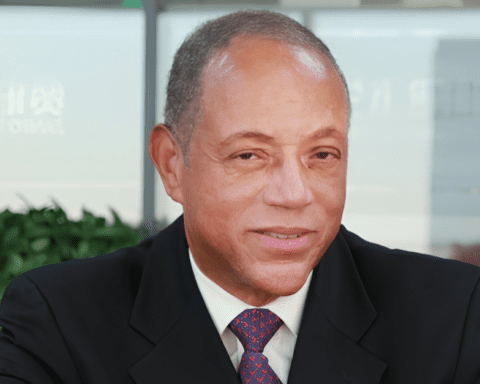

Brolly, founded by Bernard Baah, is an insurtech startup on a mission to revolutionize Africa’s auto insurance landscape.

Baah’s vision is simple yet profound: to empower Africans with accessible and affordable insurance solutions tailored to their needs. With the use of AI and a pioneering pay-as-you-go model, Brolly is transforming how drivers access and manage insurance.

In this interview, Baah shares insights into the challenges faced, the strategic vision driving Brolly’s success, and ambitious plans for expansion across the continent.

What inspired you to establish Brolly?

Fundamentally, I believe Africans have to be at the forefront of building solutions to African problems. Our best bet is to have our most qualified and experienced people going at the hardest problems whose solutions have the potential to impact millions of lives.

Insurance remains one of the most powerful human inventions to help people build economic resilience. But Africans are yet to enjoy the full benefits of insurance. After almost two decades of working at various levels in the insurance industry, Brolly is my life’s work to leverage my connections, deep market understanding, and vast knowledge and experience to help Africans benefit from insurance.

How does Brolly leverage technology to make car insurance more affordable and accessible?

At the heart of everything we do at Brolly is the human experience. We aim to make insurance easy to buy and hassle-free to claim.

We are transforming how people buy insurance by layering AI and automation to deliver insurance coverage on platforms that people find easy to use. Then we’re using machine learning algorithms to build alternative credit scoring so that we can give coverage and allow customers to pay in affordable installments.

When you ask a ride-share driver who earns daily or weekly income to pay annual auto insurance premiums upfront, you put him in a situation where he has to make difficult choices between feeding his family and paying insurance premiums. Our algorithm helps us to offer payment flexibility by using our customers’ income patterns and other proprietary data.

What challenges have you encountered while building Brolly, and how are you navigating market-related obstacles, particularly in the context of the Ghanaian insurance landscape?

The main challenges have been with the state of technology infrastructure, lack of data, and regulation.

We’ve had to take many steps back in most cases to lay the very rails on which our software needs to run. That slows you down a bit. There’s no data on the credit history of the initial market segments we’re focused on. So we have had to figure that out. And then you have the classic scenario of regulation staying behind innovation, so you run into roadblocks.

As I noted earlier, I have been privileged to work at very high levels in the Ghana insurance industry. Therefore, I usually know who to speak to when I run into regulatory obstacles. Secondly, we have adopted market transformation rather than a disruptive approach to developing our business. This enables us to build partnerships and alliances quickly.

How is Brolly differentiating itself in the insurtech space and building a strong competitive advantage?

Firstly, we are grounded on our purpose as a company “to keep drivers moving”. In that light, we’re going hard at saving our customers money and developing value-adding services on top of affordable auto insurance.

Secondly, our product and service design are natively focused on the peculiarities of our market. For example, our pay-as-you-go model is what we call “pay small-small’ and this is because the typical app-based as pay-as-you-go in Europe or America was bound to fail.

Thirdly, we have chosen a specific market segment to build for and dominate before going for other segments. This thinking is reflected in our multi-country growth plans as well.

In terms of our competitive advantages, we started with our founding team’s relevant competence and experiences as well as market understanding and connections. We are quickly building moats through key partnerships with carriers and ride-share platforms. Then, we’re providing free software tools to carriers to enable them to interface seamlessly with our platform and that enables us to build strong lock-in.

In terms of our offering to our customers as well, we’re developing additional services that deliver value on top of auto insurance. These are aimed at increasing customer lifetimes and shared value.

What are your future goals and expansion plans?

2024 is primarily focused on growing our sales and customer base in Ghana. We aim to achieve critical mass so we can fully unlock our model’s network effects to power accelerated growth. While we do that, we’re also sowing the seeds for take-off in other African countries.

We have our eyes on seven African countries over the next 3 years.

Interested in investing in Black founders? Please complete this

Interested in investing in Black founders? Please complete this