Peer-to-peer (P2P) lending is disrupting the financial industry via online platforms that provide individuals and businesses with more innovative lending and borrowing options.

Options like SoLo, a mobile peer-to-peer lending exchange that provides affordable access to low-value funds. We spoke with CEO/Co-founder, Travis Holoway to find out more about the company and its plans.

What inspired you to create SoLo?

We started this company because when we looked around our community we were disgusted by the lack of financial resources available to those who look like us. The purpose of SoLo is to combat what we feel are two of the biggest problems currently plaguing minority communities; affordable access to capital and financial literacy.

Every day more people in inner cities are being lured into debt traps from payday and title lending institutions. Since we don’t teach financial literacy in schools, people are learning their financial lessons by making mistakes which are some of the most expensive mistakes they will ever make.

Furthermore, our most noble but vulnerable citizens like single mothers, teachers, and active duty military are being taken advantage of the most. It’s promising to see that awareness is increasing in regard to the predatory payday-lending industry, but there has been no real solution until now. We intimately understand this problem because we’ve lived it, so it’s our belief that we are uniquely qualified and positioned to solve it.

What differentiates your company from the other P2P lending platforms?

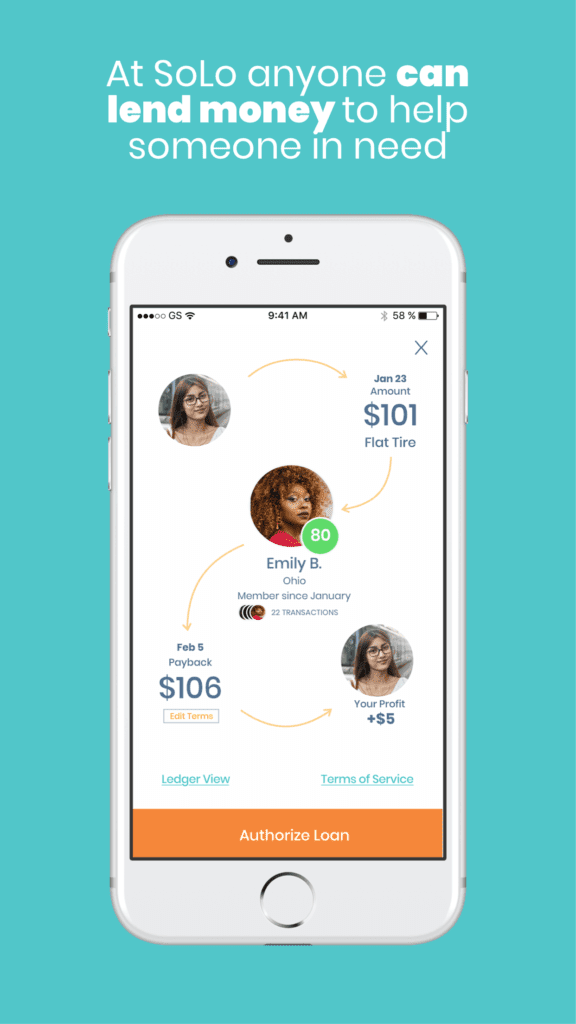

We believe that there is a misconception about what peer-to-peer lending really is. The biggest names in the industry are financial institutions that make all the financial decisions once they get money from lenders. These institutions take money from Mike and decide if Tom is an eligible borrower.

Mike has no control over how his money gets disbursed. SoLo is peer-to-peer lending in the purest form ever. We allow Mike to decide exactly who his money goes to. Other P2P platforms are solely focused on loans between $1k-40k. These alternative loans are great for some people, but not the average American.

78% of American workers are currently living paycheck to paycheck which means the majority of people are one surprise away from financial hardship. These people don’t need a $15k loan, they need $400 to get their car fixed or $100 to pay a utility bill to keep the lights on. The average payday loan borrower takes 8 loans at $375 a year. These are the people who need access to more affordable loan resources and our predecessors haven’t focused on that group, we’re here to change that.

Why would it benefit someone to borrow using SoLo as opposed to a traditional financial institution?

Traditional financial institutions are not even an option. You can’t walk into any traditional bank and obtain a loan for $75 because they don’t lend small dollar amounts.

Resources for loans under $1,000 are extremely limited which is why the payday lending industry has been able to capitalize off of our country’s most noble but vulnerable citizens.

Payday lending institutions charge 400% interest rates. At SoLo borrowers set their own terms. There are no imposed or mandatory interest rates on our platform. We are the most affordable lending option available in this country.

What measures do you have in place to protect investors who lend on the platform?

When the lender and borrower agree to terms a digital promissory note is created which states that the borrower has agreed to accept a loan from the lender and will pay back the debt. On the agreed upon repayment date, we do all the work.

The lender does not have to remind the borrower about the outstanding debt and the borrower doesn’t have to remember to repay the debt. We automatically draft the funds from the borrower’s account and return them to the lender. In the rare case that there are insufficient funds in a bank account, we will attempt to draft again at a future date. If we are unsuccessful in drafting the funds, the debt becomes eligible for collections.

The lender has the option of whether or not to send the debt to collections. If sent to collections our third-party collections provider will work diligently to recover the debt and return the funds to the lender.

What are some obstacles or challenges that you foresee and how do you plan to overcome them?

For technology companies, marketing to minority communities has proven to be challenging. With the exception of social media platforms, non-college educated minorities are often late adopters of new technology. I can recall a trip to the barbershop a few months ago when nobody in the shop had ever heard of AirBnB.

It was shocking to realize that a company that I deemed to be a “Household Name” could be virtually non-existent in the neighborhood where I grew up in. Although Airbnb is one of the most disruptive companies in the last 20 years, but it had no brand recognition in my community. It was at that point that I realized we would have to aggressively market to our target demographics.

To think that people will hear about us solely because we are scaling would be irresponsible. Historically, minority communities are skeptical of financial institutions and because of that trust must be built. It’s imperative to build an organic word-of-mouth referral culture amongst our users. I believe we will overcome this challenge if we remain transparent and cherish the trust we build with our users.

Where do you see the company in 5 years?

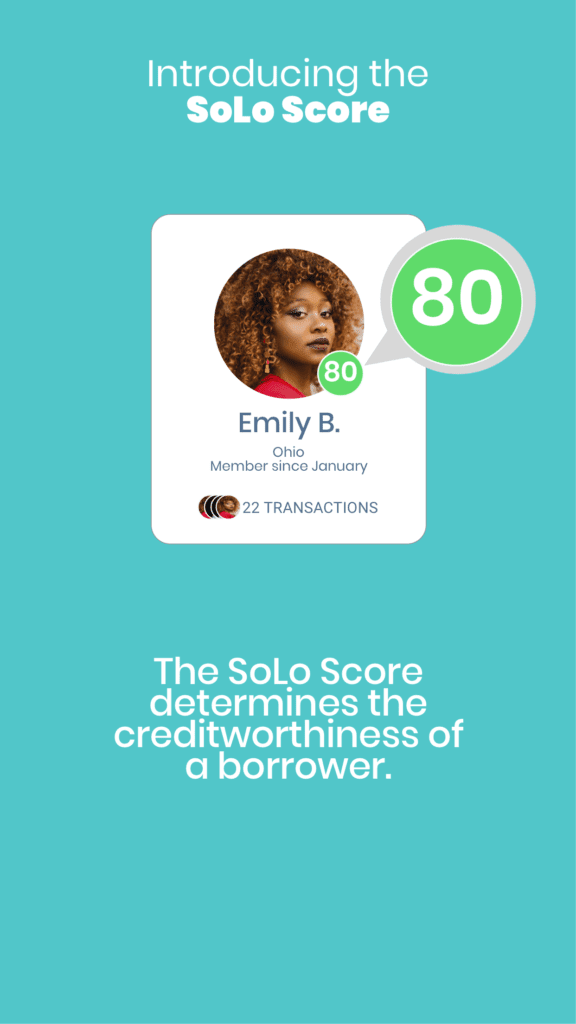

Ultimately, we see SoLo evolving into a data company. The information that we have about the underbanked population is valuable and extremely insightful because this demographic has been elusive to traditional financial institutions.

The majority of Americans have subprime credit scores and are not eligible for traditional credit because they don’t meet the stringent criteria of banks. With that said, banks will need alternative data in the future in order to make intelligent credit decisions, and we’ll have the data they need.

At what point will you consider the company a success?

I already see the company as a success. I know that sounds strange from a company in its infancy that isn’t even cash flow positive yet, but the day we launched and processed our very first loan I felt like a boulder had been lifted off of the back of that borrower. Every loan fulfilled on our platform means that’s one more loan that wasn’t taken from a predatory payday lending institution.

I’ve already received many testimonials from people who simply appreciate the fact that we exist and understand their plight. Knowing that a child had food on the table because of what we created is a win every time.

Having a positive social impact was the goal from day one so in my eyes we’ve already found success, now it’s just a matter of how many more people we can be a resource to.

What advice do you have for aspiring entrepreneurs?

You have to be all-in because it won’t work if you have one foot in and one foot out. I tried that, and it didn’t work. I used to work on the idea whenever I got extra time and I would get excited about things that didn’t matter, like a new pitch deck. That created a false sense of security because while pitch decks are important, I wasn’t truly making any tangible progress on the vision.

You learn by doing. Trust that you will find solutions to problems as they arise. Move fast because if you’re cautiously pressing the brakes, just know that someone else in the world is aggressively pressing the gas and they will beat you to the destination.

Ideas don’t come to just one person, they come to many, but few people ever see them through. Running a company is indeed a marathon and not a sprint, but marathons still have winners and losers. Be a winner.

Check out a previous interview with SoLo Co-Founder Rodney Williams – LISNR: The Black Owned Business that Raised over $10 Million and is Disrupting the Mobile Technology Industry

by Tony O. Lawson

Advertise your Business

Advertise your Business

Interested in investing in Black founders? If so, please complete this brief form.