Diagon is a company that’s redefining the way manufacturers find and purchase equipment. They offer a next-generation procurement platform that streamlines the…

More

Fashion tech startup The Folklore, founded by Amira Rasool, has secured $3.4 million in seed funding. The fresh capital brings their total…

More

Atlanta-based startup Cookonnect is whipping up a recipe for success, having recently secured a $1 million pre-seed funding round from Los Angeles-based…

More

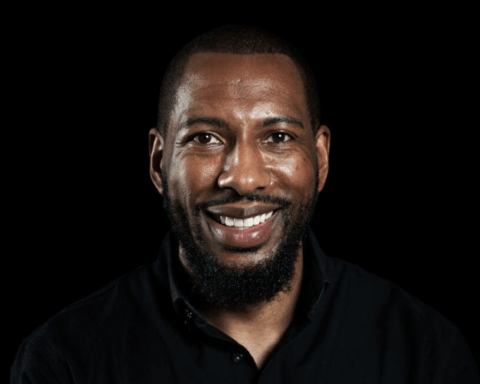

As the Managing Director and Head of Starwood Impact Investors (SII), Bakari Adams leads a return-driven investment platform dedicated to investing in…

More

New York Life, the nation’s largest mutual life insurer, announced today that it has acquired a minority stake in Fairview Capital, one…

More

City Girls Golf is an organization founded with the mission of empowering women of color through the game of golf. Founded by…

More

As spring sunshine warms the days, it’s the perfect time to shed those winter boots and update your footwear wardrobe. Look no…

More

As the sun peeks out and the days get longer, it’s the perfect time to refresh your wardrobe with some spring staples.…

More

Discover an array of exquisite jewelry from Black owned sustainable jewelry brands that offer unique and eco-friendly designs. These businesses create stunning…

More

Mark Dusseau’s journey through the foster care system has instilled in him a deep commitment to social impact. His company, Dusseau and…

More

The Corporate Transparency Act (CTA), passed in 2020, has stirred up significant discussion and some confusion regarding its implications for business owners,…

More

As the Baby Boomer generation prepares for retirement, a vast, untapped potential emerges: established, profitable businesses seeking new ownership. This presents a…

More

Building a strong financial IQ is critical, yet a significant portion of the global population faces challenges in this area. This lack…

More

In the world of finance, the adage “it takes money to make money” often rings true. For the ultra-wealthy, one of the…

More

From the Bipartisan Infrastructure Law to major industry deals like Blackrock’s $12.5 billion acquisition of infrastructure investment firm Global Infrastructure Partners, several…

More

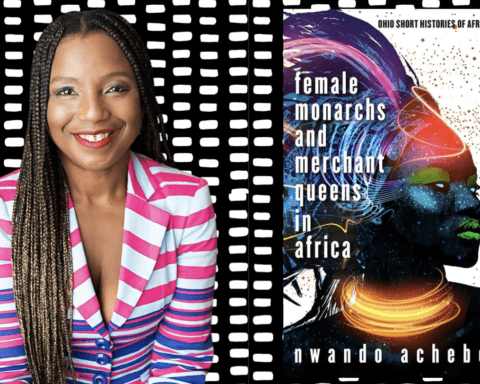

For centuries, the narrative of African leadership has been dominated by male figures. But the book, “Female Monarchs and Merchant Queens in…

More

For too long, the image of the cowboy has been a singular one – a white man on a horse, conquering the…

More

For over five decades, Bernard and Shirley Kinsey, alongside their son Khalil, have woven together a remarkable tapestry of African American history…

More